DeFi portfolios

Portfolio categories

Levva operates several permissionless vaults to demonstrate its portfolio technology and attract both professional and non-web3 native users. At Levva, we are strong proponents of a systematical approach to managing liquidity on-chain, which is why we’ve come up with defi portfolio vaults.

Each defi portfolio vault serves the needs of a certain user category in crypto. We categorize users by their individual risk preferences:

Ultra safe

Risk tolerance: Low. No access to leverage. Example: HNWI, fund, or a person who is just getting familiar with web3 and DeFi. Such users are looking for a simple “one-click” exposure to DeFi yields and are only comfortable with blue-chip lending or staking protocols (e.g., Aave, Lido, Morpho). The simpler the setup and the fewer counterparties involved, the better.

Safe

Risk tolerance: Low to Medium. No access to leverage. Example: A person who is familiar with DeFi and knows about the risks associated with web3 and crypto in general. He has tried several DeFi protocols and DEX-es. In addition to lending protocols, safe users may consider providing liquidity in AMMs or holding yield-bearing assets and stablecoins.

Brave

Risk tolerance: Medium to High. Has access to leverage. Advanced crypto and DeFi user who understands risks inherent to blockchain and smart-contracts, does his own research when allocating into certain protocols, vaults, pools, and strategies. Uses multiple blockchains and bridges. May occasionally use leverage through lending market loops to farm yield or points. Can get exposure directly to yield-bearing assets or RWAs. Uses protocols such as Pendle, Curve, Uniswap, Aave, Morpho, Euler, Gearbox, Etherfi, Syrup, Synthetix, Ethena, Fluid, GMX, e.t.c.

Degen

Risk tolerance: High. Uses leverage often. A typical speculator who trades either spot or perp markets with leverage. Prefers expectation of ultra-high rewards in return for taking margin risk. Risks loosing his entire trading/gambling portfolio. Trades on Hyperliquid, GMX, pump.fun and similar venues. Additionally may use prediction markets and/or snipe meme-coins or illiquid assets which require prompt actions when trading/handling. Usually chases opportunities with potentially high rewards without ever looking back at risk specifics or nuances. Usually has a much lower capital than the above 3 categories.

DeFi portfolios

Levva defi portfolio vaults allocate capital into different tokens and DeFi protocols. In Levva we treat all non-stablecoin token exposure as volatile assets (e.g. stocks) and all of the yield exposure (lending, yield-bearing stablecoins, stable AMM liquidity provision) as safer assets (e.g. bonds). Armed with this simple TradFi analogy we can embark on the interesting adventure of portfolio optimisation techniques.

Simple portfolio model

To keep things simple, we will consider a 2-asset model: ETH as a volatile asset and Aave v3 lending yield as a safe asset. This is a very good proxy model for dealing with portfolios in EVM-based chains. Given the high correlation and volatility nature of most on-chain assets, this model represents a broad range of use-cases we can cover with defi portfolios, as we can statistically treat both volatile and safe assets as identical to each other.

| Allocation | Expected return, ann. | Volatility, ann. |

|---|---|---|

| ETH | 15% | 60% |

| Aave | 5% | 4% |

We also know that average correlation level between ETH and Aave yield has been 0.2 for the period considered. We now have all of the variables to evaluate 3 different portfolios:

| Portfolio | ETH weight | AAVE weight | GM return | Volatility | Sharpe |

|---|---|---|---|---|---|

| Maximum SR | 0.00% | 100.00% | 4.92% | 5% | 1.25 |

| Risk parity | 6.25% | 93.75% | 5.46% | 5.81% | 0.97 |

| Maximum GM | 27.5% | 72.5% | 6.25% | 17.31% | 0.44 |

Key observations

- This should be a revelation for many: even ETH as an asset is considered to be a super risky investment, and shouldn’t constitute more than 27.5% of one’s portfolio.

- The maximum Sharpe ratio portfolio puts all weight in the low-volatility asset (Aave) because the increase in expected return of ETH (3x higher) doesn’t compensate for its much higher volatility (15x higher).

- The maximum geometric mean portfolio takes on more risk, allocating about 27.5% to the high-volatility asset, yet the risk is almost 4x smaller than the risk of ETH. This is because:

- The geometric mean considers both growth and risk

- The higher expected return of ETH contributes to long-term growth

- The optimal portfolio finds a balance where additional expected return justifies increased volatility

- The risk parity portfolio naturally adjusts for large volatility differences (60% vs 4%)

- The low correlation of 0.2 between assets helps improve the geometric mean portfolio’s risk-adjusted performance through diversification, but isn’t enough to overcome the extreme volatility difference for the Sharpe ratio portfolio.

Practical implementation.

Protocols and assets

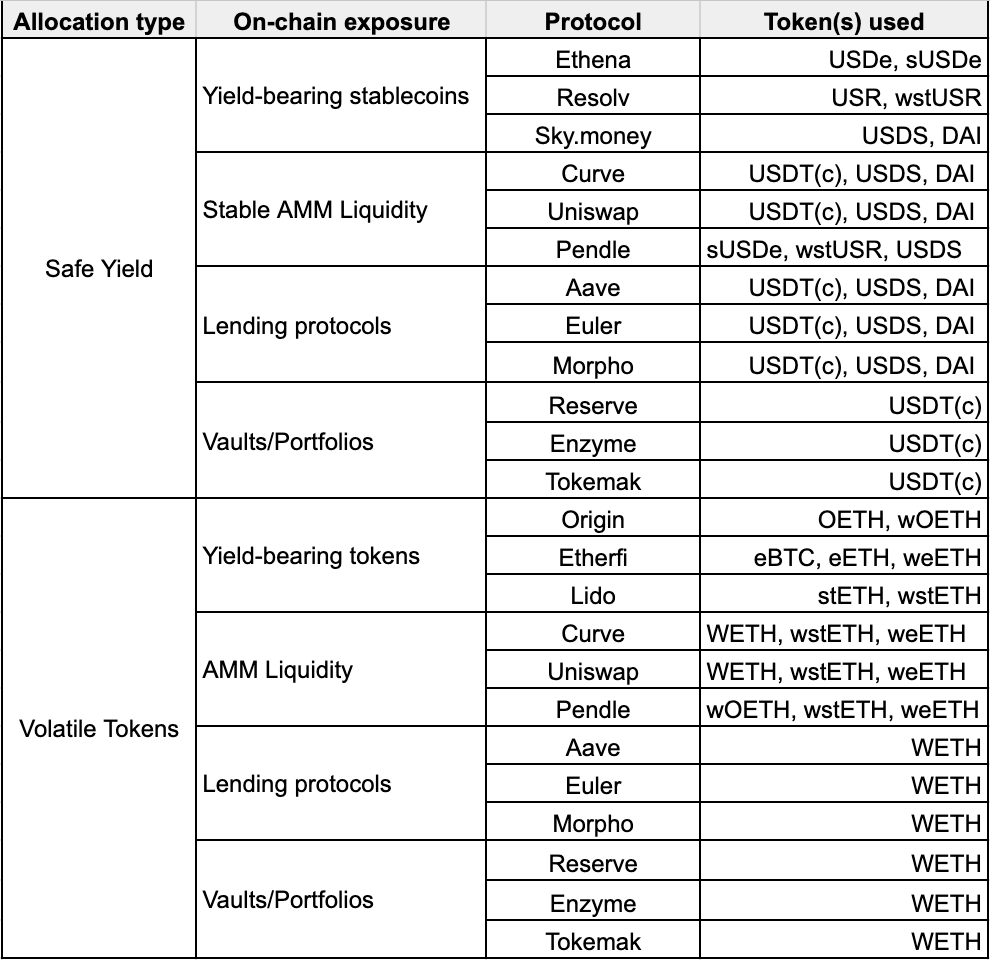

Below is the comprehensive breakdown of the protocols and tokens used to form DeFi portfolios for permissionless vaults operated by Levva. We constantly expand the universe of our DeFi protocol adapters to offer ever broader yield opportunities and allocation options for our customers.

Note the composability depicted in the table: For example, one of the valid allocations for a certain Levva vault could be a provision of liquidity to a Curve’s stETH/WETH pool, combined with some safer yield option like Reserve’s or Tokemak’s stablecoin diversified DeFi portfolio.

Users or funds who deploy personalised vaults may further configure protocol and asset whitelists using their own preferences. This includes flexibility in setting their own allocation weights.

Market Timing

Levva’s portfolios which get exposure to volatile asset allocations may be further improved by timing the market: we automatically scale (hedge) in and out of the volatile position depending on what market momentum indicators have to say. We are primarily focused on a medium-term momentum and consider 10 - 30 day sliding windows when working with historical data. This is a sweet spot in terms of rebalancing frequency to control costs, and profound market effects or autocorrelation that one may capture.

Several scaling (hedging) techniques are available:

- Sell volatile asset into yield-bearing stablecoin (e.g. increase safe yield allocation).

- Use volatile asset as collateral, sell perp contract on the same underlying.

- Use volatile asset as collateral, borrow underlying, sell short on DEX.

Strategy swarms

Market timing allocation strategies perform best when they work in tandem with similar instruments. These so-called strategy swarms may represent different momentum or mean-reverting trading techniques with variable lookback periods and other parameters. The swarm helps capture market effects like momentum and mean-reversion on different time-scales.

We then can use optimization techniques across the strategies in a similar way we optimise across assets: each strategy gets its own weight depending on how well it performs and how closely it correlates with other strategies.